Timing the housing market is probably one of the hardest forms of investing due to the illiquid nature of real estate and data lag that is associated with it. With the recent run up in real estate prices, many people have been bemoaning the fact that they missed the market bottom. Well, according tho this article by market watch, read it here, you’re in luck if you’re looking for real estate in Illinois, New York, Florida or any one of the 23 judicial states, that is any state which requires a judge to review the foreclosure before it can be finalized. So there is hope yet in snagging the bottom in these states.

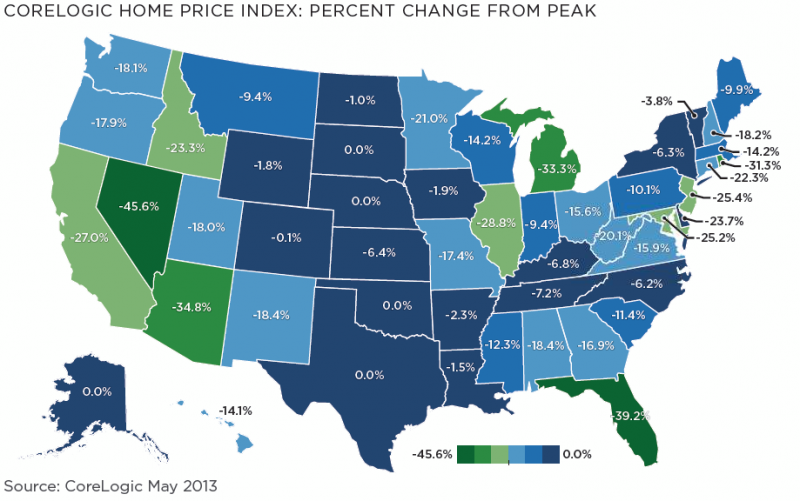

There has also been talk that we’re entering another housing bubble due to the recent run up in prices. Personally, I don’t think we’re in real estate bubble territory yet. My belief is we’re essentially in year 2 of a 6 year real estate market cycle and still some ways from peak prices. I am estimating we are still a good 25% away from peak prices based on the transactions I am following here in Orange county. I believe my view is supported given the level of optimism among new home builders, who essentially are projecting 1-3 years into the market ahead due to the time lag between building and a new owner actually taking the keys to the new home. To see more infomariton about the growth in the number of new home starts and permits, check out the link here.

For more in depth statistics on where the real estate market is right now, check out the link here. One of the interesting tidbits from the article was this

“History shows that a rapid rise in interest rates tends to have little correlation with home prices. Rather, rising rates are more likely to contribute to a decrease in home purchase volume and an increase in the market share of adjustable-rate mortgages,” wrote Mark Palim in a Fannie Mae commentary.

Logically, it seems like interests rates would have an effect on home prices, especially since interests rates affects volume as mentioned above. Perhaps it’s one of those strange statistics that we need to uncomfortably accept?

[Edit] With the recent rise in interests rates, mortgage application have fallen significantly. This plus the tighter lending standards, and spread between current prices and past peaks leads me to believe we are still not in real estate bubble 2.0 yet. A more detailed write up can be seen here.

[Edit] Here’s another article that illustrates well the difficulty of timing the real estate market. Read it here.